Apps like Moneylion that Help you get Money Fast

(Competitors & Alternatives)

Tina graduated from Ohio University with a Degree in Business Management. She comes to us with several years of experience in Retail Management and has helped us scale our Retail Glossary and Information department on DigitalConsumer.org. She uses almost every single Mobile Payment solution, including Apple Pay, Cash App, Venmo, Zelle, etc and is well-versed in writing articles and researching retailers, businesses and companies that use these technologies. She enjoys writing about new technologies in the retail, software, technology and business sector.

DigitalConsumer.org has the resources, staff, expertise and background to help people make informed financial decisions and choices. We've pooled our 25 yrs of combined experiences to ensure we can bring you the most unbiased, well informed content on the internet to help you make the right choices when looking to better your life.

DigitalConsumer.org adheres by strict editorial guidelines - Our readers can rest assured that we’re putting their interests as our top priority. Our articles and content is reviewed and written by industry professionals and edited by qualified subject matter experts, who further ensure all content or topics we publish is accurate, unbiased and trustworthy.

Our skilled contributors and reviewers emphasis their research and data analysis to align with what our readers want and need to learn more about - This includes (but is not limited too) making money on the side, finding information about retailers & online stores, how to earn income on the side and many other subjects of this nature. We strive to help everyone feel confident with their decisions and endeavors.

DigitalConsumer.org adheres by strict editorial guidelines - Our readers can rest assured that we’re putting their interests as our top priority. Our articles and content is reviewed and written by industry professionals and edited by qualified subject matter experts, who further ensure all content or topics we publish is accurate, unbiased and trustworthy.

Our Mission & Principles

We take pride in making it our mission to provide authentic, accurate and unbiased content, articles and data analysis of products and services for our readers. We've set high editorial standards to ensure that we meet and exceed the expectations of adding value to our readers' lives through our recommendations, reviews, comparisons and information. Our review and editorial board fact-checks all content maintain accuracy and integrity before our content is published to uphold our editorial standards. In order to not influence our editorials and contributor teams, we ensure that our contributors and editorial teams do not receive compensation directly from our advertisers.

Editorial Independence

DigitalConsumer’s contributor team and review board has one goal - To give our readers the most unbiased and honest advice to assist in making personal finance choices and decisions - Whether you're looking for services and apps to make extra cash on the side or finding a retailer or business to work with. We've enforced strict editorial guidelines to ensure that information and content presented to our readers on our website is not influenced by our advertisers. As mentioned above, our team of writers, contributors and editors receive no direct compensation from our advertisers, and our articles, content and reviews is properly fact-checked to ensure 100% accuracy.

Our expert team of contributors, writers and review board have a combined experience of over 25 yrs in business, finance and retail. We pride ourselves in helping our readers stay informed on consumer finance, business and retail information.

DigitalConsumer.org adheres and follows strict editorial guidelines, to ensure our readers can trust that our articles, content and reviews are unbiased, accurate and trustworthy.

Digitalconsumer.org is Independently owned, advertising-supported publisher and comparison internet service. We are compensated from advertisers to place ads (in-content, sidebar, and header ads)or by you clicking on affiliate links posted on our website. This compensation may impact where, how and in which order products are listed within categories or in our content. While we continually update and strive to showcase a wide variety products, services and offers, DigitalConsumer.org does not include content or info about every Product, retailer, service or app.

We’ve probably all come across a time in our life when we needed a little extra cash.

If a situation should ever arise that makes it hard to acquire cash immediately, there are a few options for borrowing money without going bankrupt.

For example, apps like Brigit and MoneyLion are apps and services that allow you to borrow money before your next paycheck arrives.

The Brigit app is accessible for free however, a $9.99 per month “Plus membership” package has additional features.

MoneyLion, with an APR ranging from 5.99 percent to 29.99 percent, may turn off a lot of individuals but, it does also have a lot to offer.

Because no lending app is the same, we have 15 different choices in today’s post to help you review the various options.

Here’s the Best Apps like Moneylion that Help you get Money Fast:

Earnin

Earnin is an app that allows users to have access to their before their actual payday.

This gives users the ability to pull money from their paycheck early should they need some extra cash in a pinch.

You may cash out up to $100 every paid month with the app Earnin.

Commissions, fees, and subscriptions do not exist on the Earnin app, which is even better, but the platform will be tip-reliable.

You can tip directly within the app.

When you borrow money against your paycheck, Earnin will simply deduct that same amount once your paycheck is actually deposited on payday.

If you want to be able to access your paycheck early, Earnin is here for you.

Another useful feature about this app has is that it alerts or notifies, or warns its users whenever the balance is below $0-$400, which may help you manage your money more effectively.

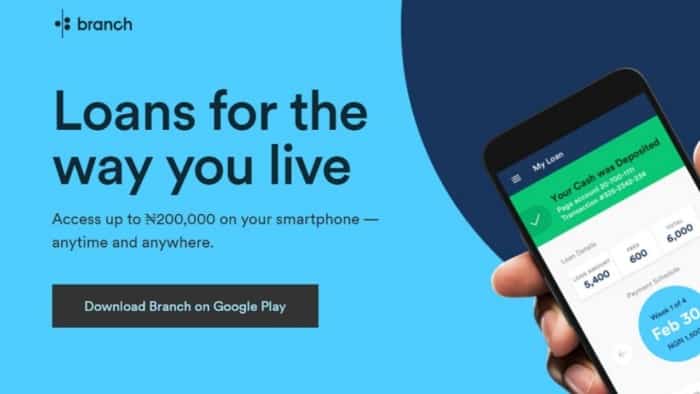

Branch

Apps like Brigit, MoneyLion, and Earnin are not on service to all countries; some apps and services are primarily concentrated in the US.

So, what is the next thing to do?

The app Branch is available to residents of Tanzania, Kenya, Mexico, India, and Nigeria.

The app Branch offers loans with a monthly interest rate for up to 48 weeks.

The interest rate changes depending on the region, so double-check what the rates are in your area.

From your smartphone, you may request and receive any loan.

An app that focuses more on traditional loaning services, that’s what the app Branch is focused on, unlike Earnin.

As a result, the app Branch’s price is somewhat higher.

Dave

The previously mentioned app, Earnin, is similar to the app Dave in that it allows you to access your salary up to $100 in advance of payday.

Although the two services are nearly identical on the surface, there are a few key distinctions that may make Dave more interesting to you.

Dave has teamed up with LevelCredit to submit your loan payments to the central credit agencies.

This means that the Dave app can help you establish or increase your credit score.

One other significant distinction is that Dave is a one-time $1 per month fee.

However, this isn’t excessive, and we don’t believe that the premium membership will deter many people from joining the Dave app.

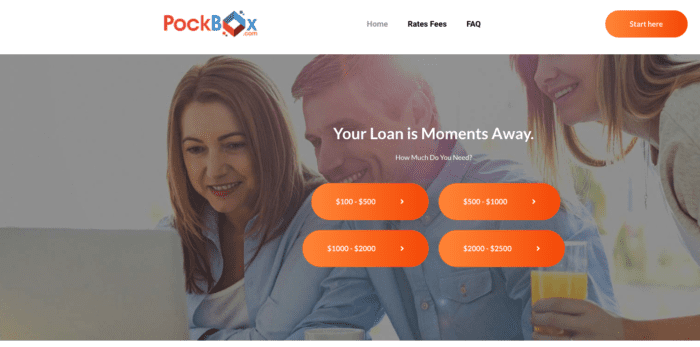

PockBox

PockBox is a more traditional lending business that allows you to obtain up to $2,500 in loans with monthly interest.

Another essential thing you have to know about PockBox is that it is not a loan-provided app, but it can connect you to its lenders.

As a result, you have more options when it comes to selecting a loan.

Not just that, even if users have terrible or have no credit score, they will still be able to access its lenders that willing want to provide loans.

We have no way of knowing how much interest you’ll have to pay because it all relies on the lender, so you will have to apply for yourself to find out.

CashNetUSA

Throughout the United States, CashNetUSA provides payday and installment loans.

Because loan rates and conditions differ from state to state, you need to check CashNetUSA’s website.

CashNetUSA’s primary service is payday loans.

These loans are typically due on your next paycheck but extensions of loans may also be available in some areas.

You may get a loan no matter what your credit score is, and that’s what makes CashNetUSA great.

Your FICO score will not be affected, and that is because CashNetUSA does not submit loan information to Equifax, Experian, or TransUnion.

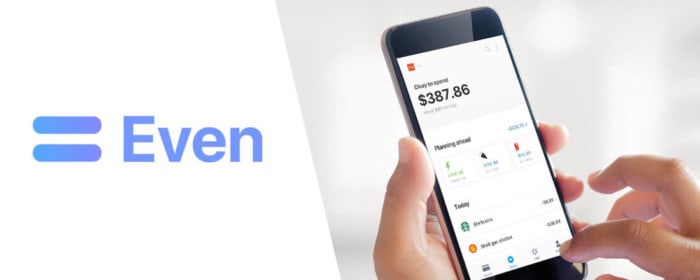

Even

The Even app has worked with consumers around the US to provide early access to earnings.

The program essentially allows you to get early cash rewards that are debited from your paycheck.

The terminology is somewhat different, even if it is similar to the app Earnin in this regard.

For an $8 monthly fee, you can make on-demand payments whenever you like.

$8 a month isn’t much, especially if you’ll be requesting money several times over the month.

We offer a couple more alternative options further down the page if $8 a month is too much for your budget.

You should verify with your employer to see if you are eligible for Even payments.

That’s another thing to keep in mind with programs like Even is that your employer must be a partner.

Chime

If Earnin or Dave’s concepts appeal to you more than Even’s, Chime is a viable option.

Like Dave and Earnin, Chime pays out early on paychecks, but in a slightly different method.

You will receive a Visa Debit Card as well as a Spending Account if you choose to engage with Chime.

Chime has a nationwide system from over 38,000 ATMs where you can transfer up to $500 each day without incurring any fees.

Interchange fees, which are charged on every card transaction, are how Chime generates money.

You may utilize the service for free, but will be charged with each transaction.

$2.5 will be charged to you per payment if you receive money from a Bank account that’s not a part of Chime’s ATM network.

However, because Chime is connected to over 38,000 ATMs, you must be likely to dodge this cost with ease.

You may also use Chime to save income, which you can do through a Savings Account that is optional.

Avant

The Avant app has two kinds of services to offer:

· With a 24.99 percent -25.99 APR, credit cards with credit limits of $300 to $1,000 are available. A yearly cost of $29-$59 is charged for this service.

· Personal loans that are unsecured and secured.

You might receive better conditions and a faster loan approval if you use your automobile as collateral.

Also, secured loans mean fast cars.

Your state determines the exact fees and terms.

However, these are the conditions of Avant in general:

· Unsecured loans range from $2,000 to $35,000, while secured loans range from $5,000 to $25,000.

· Unsecured loans have a term of 24-60 months, whereas secured loans have a term of 24-48 months.

· Unsecured loans have an administration cost of up to 4.75 percent, whereas secured loans have a fee of 2.5 percent.

· The APR ranges from 9.95 percent to 35.99 percent for both secured and unsecured loans.

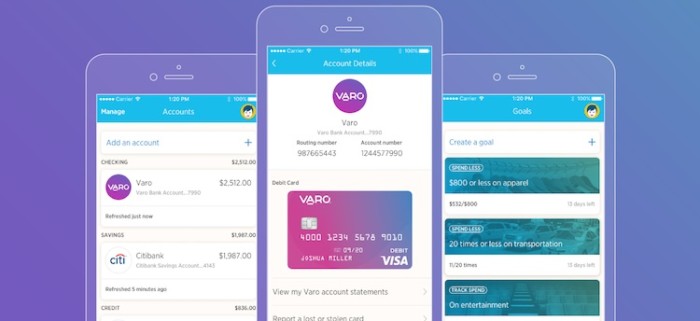

Varo

Varo is amongst the most comprehensive and precise digital banking solutions we’ve come across.

Its menu includes the following items:

· Saving accounts.

· Bank accounts.

· Checking accounts.

Varo’s bank account section is rather intriguing since it provides:

· No fees transferred.

· No withdrawing fees for more than 55,000 ATMs.

· No fees per month.

· Payments do not include overdraft over $50.

· No transaction fees for other countries.

Varo also offers personal loans ranging from $3,000 to $25,000, ranging from three to five years.

The annual percentage rate (APR) ranges from 6.9 percentage points to 23.9 percent.

Please remember that Varo does credit checks on loans, so these loans may not be available to everyone.

PayActiv

PayActiv is similar to Even in that it has worked with firms throughout the United States to allow employees to receive their paychecks early.

Furthermore, your paycheck is withheld for all withdrawals.

Also, not every company may be a PayActiv partner, so you may not even be able to access it.

Even PayActiv has significantly different names, even though the fundamentals are essentially the same.

If you utilize PayActiv, you will only be charged the bi-weekly amount; otherwise, you will not be charged anything.

Also, PayActiv allows you to deposit up to $500 and charges you $5 every two weeks.

Bear in mind that certain employers may only cooperate with these two platforms. So, in addition to the cost, think about the service’s availability.

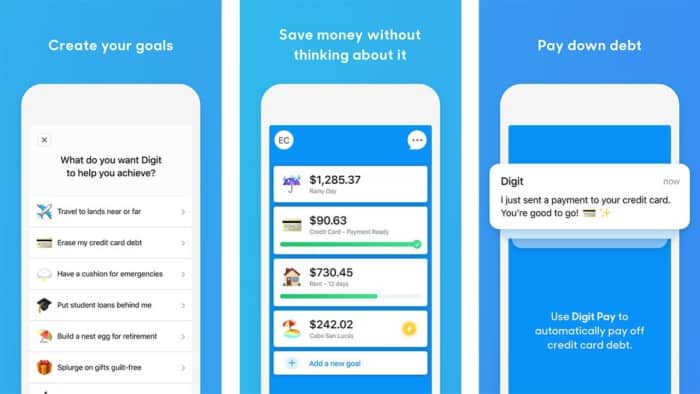

Digit

An app that is a little different from the other services that have been listed, that’s what Digit is.

Digit’s goal is to assist its users in saving more money.

Digit is first on this list to focus purely on saving, even though we’ve seen loan services with optional savings elements before.

Digit works by monitoring your expenditures and moving money from your bank account to your Digit wallet once you have some leftover cash.

You’ll also earn a 0.5 percent savings incentive every three months.

Your money should be safe because all Digit accounts are FDIC-insured up to $250,000.

Unlike other savings accounts, it adjusts to your expenditure automatically and saves a lot of money without you having to do anything, and that’s what makes Digit a great app.

Like the other apps mentioned, Digit does not provide payday lenders or early salary checks.

It does allow you to save money over time, which is ideal if you have a positive net income.

Also, Digit is not that expensive to use.

It costs only $5 each month.

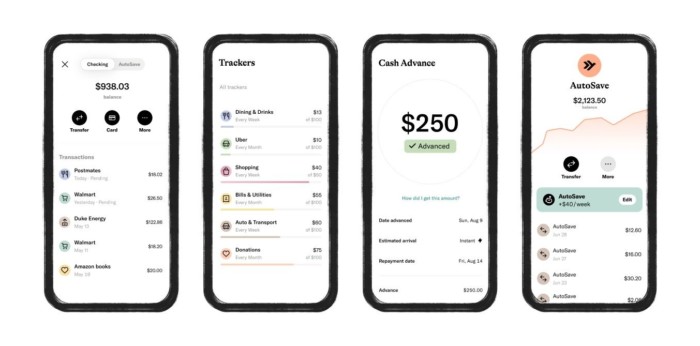

Empower

Compared to standard checking accounts, Empower is a more cost-effective option.

The app’s main advantages are as follows:

· No fees overdraft.

· Transaction fee for only 1%.

· Non-existent minimum deposit amounts.

· No need to pay for card replacement.

· Up to 0.25% of APY.

· Monthly repayment 3 ATM fee.

Empower also provides automatic investing, budget tracking and notifications, saving advice, including advance cash up to $150 in addition to these features.

Cash advances are available without a credit check and with no fees, while Empower does consider monthly average automatic payments and other variables when determining applicants’ availability.

Unfortunately, Empower isn’t free; this will cost $8 per month, with the first 30 days of being free.

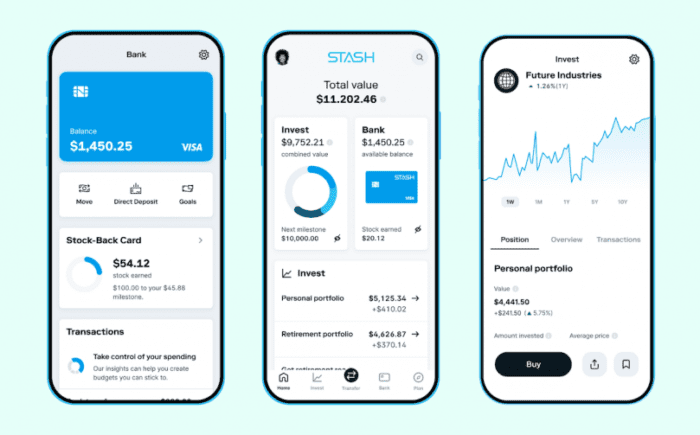

Stash

The Stash platform offers a variety of services, including up to two days early paydays.

Stash may offer its users instant access to your money when your business or benefits provider tells Stash of an upcoming deposit.

Also, $50 will be given to you for investing, but only if you do a direct deposit higher than $300 in between the 30 days.

Stash has a unique function when it comes to investing. If you’re using Stash’s Debit card to make purchases, you will be given shares.

Stock-Back is a feature that gives you 0.125 percent back on your purchases, with specific merchants offering up to 5% back.

Traditional IRA and Roth accounts are both accessible thanks to Stash.

Starting at $1 per month, Stash is also reasonably priced.

The most basic Beginner plan gives you access to all of Stash’s features, but the Stash+ ($9/month) and Growth ($3/month) plans include features like tax advantages for retirement savings and 2x Stock-Back.

SoLo Funds

Within durations ranging from 14 to 30 days, SoLo Funds will allow its users to all borrow some loans up to $1,000.

SoLo Fund is a platform that links you with lenders; it does not offer any rates or terms; these must be negotiated upon for both you and the borrower.

When it comes to lenders, SoLo Funds is unusual since it enables you to lend money as well!

As a result, this isn’t just a lending platform; it’s also a platform for money-making.

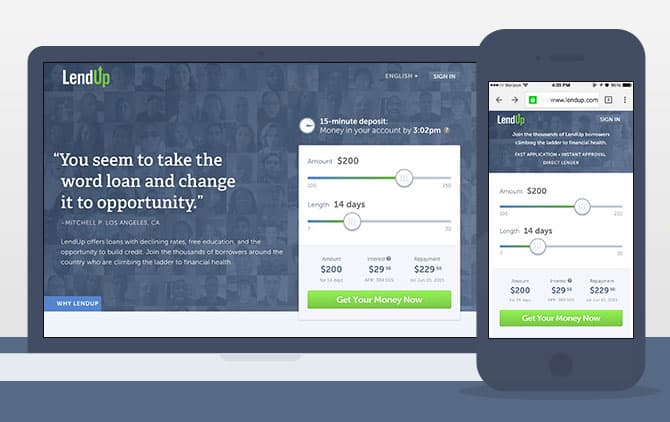

LendUp

Last but not least is LendUp.

The app LendUp is only available in seven US states, as well as its conditions and charges vary based on where you reside.

Loans for first-time users are typically restricted to roughly $250 and have terms of 7 to 30 days.

The APR fluctuates, while it often runs from 100 percent to 200 percent, with rare instances exceeding 1,000 percent.

Because the app LendUp doesn’t demand an excellent credit score to make loans, the high APR isn’t as bothersome.

If you live in Louisiana, California, Missouri, Mississippi, Tennessee, Wisconsin, or Texas, LendUp might be a great way to borrow money.